Numerical Evaluation of Adverse Effects of Economic Fluctuations on the Investment Returns of Insurance Industry in Nigeria

C. Chibuisi1*  , M. E. Egwe2 , B. O. Osu3 and C. Y. Ishola4

, M. E. Egwe2 , B. O. Osu3 and C. Y. Ishola4

1Department of Insurance, University of Jos, Jos, Nigeria .

2Department of Mathematics, University of Ibadan, Ibadan, Nigeria .

3Department of Mathematics, Abia State University, Uturu, Nigeria .

4Department of Mathematics, National Open University, Nigeria .

http://dx.doi.org/10.13005/OJPS09.02.10

The investment landscape in Nigeria is inherently influenced by economic fluctuations that pose substantial challenges and opportunities for investors and policyholders. This paper aims to investigate and provide solutions to the adverse effects of economic fluctuations on the investment returns of Insurance Industry in Nigeria through a numerical evaluation. These adverse effects are capable of resulting into future delay and volatility-noise of economic fluctuations in the financial market which influences the investment returns of Insurance Industry. These adverse effects are modeled as Advanced Stochastic Time-Delay Differential Equation (ASTDDE). The modeled equation is solved using a two-step Hybrid Block Adams Moulton Methods (2HBAMM) with the help of new sequence for delay and noise terms computations. Numerically, through mathematical demonstration, these adverse effects are expressed in form of some examples of Advanced Stochastic Time-Delay Differential Equation (ASTDDE) and were solved using the proposed method which revealed its financial and economic implications.

Copy the following to cite this article:

Chibuisi C, Egwe M. E, Osu B. O, Ishola C. Y. Numerical Evaluation of Adverse Effects of Economic Fluctuations on the Investment Returns of Insurance Industry in Nigeria. Oriental Jornal of Physical Sciences 2024; 9(2).

DOI:http://dx.doi.org/10.13005/OJPS09.02.10Copy the following to cite this URL:

Chibuisi C, Egwe M. E, Osu B. O, Ishola C. Y. Numerical Evaluation of Adverse Effects of Economic Fluctuations on the Investment Returns of Insurance Industry in Nigeria. Oriental Jornal of Physical Sciences 2024; 9(2).Available here: https://bit.ly/4hmnafQ

Download article (pdf) Citation Manager Publish History

Introduction

In 1,2, Economic fluctuation refers to the variations and unpredictable changes over a stochastic period in economic activities which are influenced by a complex interplay of economic factors such as turbulence in inflation rate, human development index, volatility in gross domestic product (GDP) of a country due to fire-brigade approach in new policy implementations and currency-exchange rates. These economic fluctuations can occur over various time frames, ranging from short-term to long term shifts in economic trends of insurance industry in Nigeria. 3 Insurance is defined as a contract in which the policyholder pays a certain amount of money called premium to the insurance company for insurance coverage against any potential loss. According to 4, the live wire of an insurance industry depends on the premium payment by its policyholders. One notable aspect of economic fluctuations in the insurance industry which encompasses the alternating periods of expansion and contraction in its economic activities is the level of patronage by their policyholders. In 5,6, one major macroeconomic factor that determines the level of patronage insurance industry received for its services and products depends on the protection of policyholders’ trust which influences its investment returns. During an expansionary phase, the investment of an insurance industry experiences growth in return which reveals the high level of trust and patronage shown by its policyholders in purchasing the insurance policies and payment of premiums. Conversely, during a contraction or recession, the investment returns of the insurance industry declines resulting in inadequate claims resolution by the insurance industry which affects the policyholders trust. The expansionary and contraction phase for alternating investment returns of the insurance industry depends on the policyholders trust and patronage which result to advanced stochastic economic movements or volatility. 7,8 revealed that macroeconomic indicators such as policyholders lack of trust and patronage, inflation rates, currency exchange rates, gross domestic product (GDP) growth rates, stock market indices, human development index, unemployment rates and fiscal policy measures influences insurance industry investment returns which result to future adverse effects of low premium payments by policyholders, decrease in the insurance industry profitability, delay in claims resolution, regulatory penalties and fines, loss of policyholders trust and loyalty. The existing literatures in this concept revealed that no research has been carried-out mathematically in addressing the adverse effects of economic fluctuations on the Investment Returns of Insurance Industry in Nigeria which left a huge research gap. There is an urgent need to understand, evaluate and manage these economic fluctuations which are very crucial for policymakers, policyholders and for businesses to navigate the dynamic economic landscape effectively and also to recommend best ways to reduce its adverse effects on investment returns of insurance industry in Nigeria.

To tackle these adverse effects of advanced stochastic movements in key macroeconomic indicators which causes economic fluctuations and influences the investment returns of Nigerian insurance industry resulting into adverse effects of future delay and volatility-noise in the financial market, this study applied two-step Hybrid Block Adams Moulton Methods (2HBAMM) in solving some Advanced Stochastic Time-Delay Differential Equation (ASTDDE) with new sequence for delay and noise terms computations. 9 defined ASTDDE as a stochastic process that depends on the current state and the future uncertainties. A volatility term is an uncertainty event of any probability variables {Xt,t E T}

![]()

Adapting equation (1) the constructs of this study were taken into consideration, then the modeled equation for this study becomes;

![]()

where u(t)

In the quest of obtaining the numerical solution of ASTDDE, most scholars such as 12, 14 used interpolation approach in computing the lag and volatility terms of ASTDDE for approximate solutions and suffered difficulties in obtaining the Minimum Absolute Random Errors (MAREs) at the Lowest Computer Processing Unit Time (LCPUT) which affected the accuracy of their numerical solution. 15 obtained the analytic solution of a deterministic and stochastic model of a time-varying investment returns with random parameters and revealed that the lower the absolute random errors of a stochastic process, the lower the risk effect of economic fluctuations in any financial model. The difficulty detected by the above researchers and adverse effects of economic fluctuations on the investment returns of insurance industry caused by macroeconomic indicators left a huge research gap which needs to be filled which is the motivation behind this study. To reduce these adverse effects of economic fluctuations and to overcome the difficulty experienced by the researchers in the application of interpolation approach for computation of the lag and volatility term, new sequences modelled by 16 were used. This can be done by solving numerically some examples of the modeled equation using the proposed method.

Research Method

Formulation of the Method

The discrete schemes of the two-step Hybrid Block Adams Moulton Methods (2HBAMM) were derived by 17 through matrix inversion techniques on the k-step multistep collocation method developed by 18 and presented as;

Evaluation of Fundamental Properties of the Proposed Method

Following the steps developed by 19, 20 the fundamental properties for the convergence and stability of the proposed method are examined.

Order and Error Constant

As the proposed method is one of the families of Linear Multistep Method, 19analyzed that LMM is said to be of order p

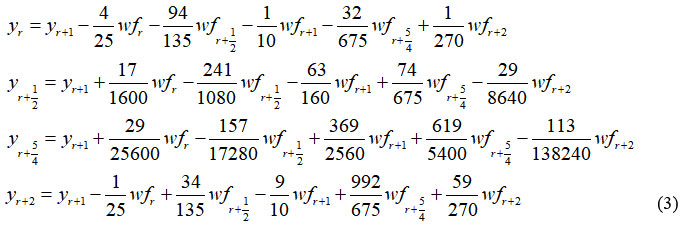

The order and error constants for (3) are analyzed and presented as follows;

Therefore, (10) has an order, o = 5

Consistency

According to 19, a Linear Multistep Method is said to be consistent if the order

Zero Stability Analysis

In 20, the zero-stability of a LMM is satisfied if no roots

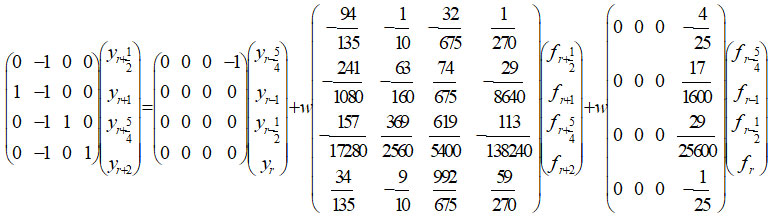

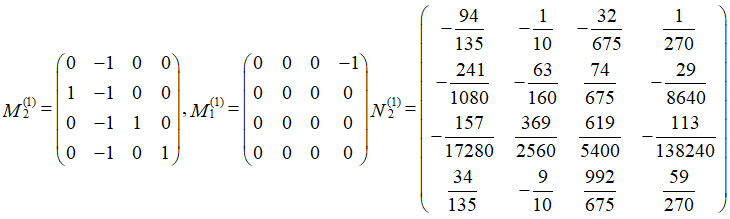

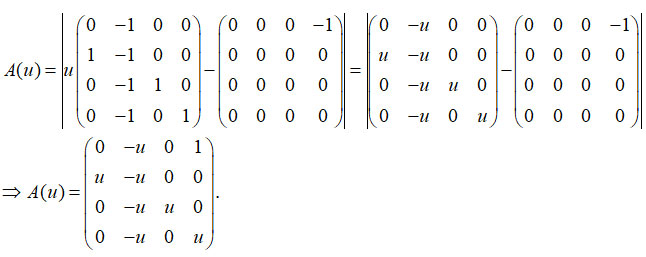

The zero stability for (3) is determined as follows:

where

![]()

Now we have,

Using Maple (18) software, we obtain:

![]()

![]()

Convergence

Following that the discrete schemes (3) of the proposed method are both consistent and zero stable, the method is convergent.

Region of Absolute Stability

The P

| Figure 1: Region of |

| Figure 2: Region of |

Numerical Implementation and Computations

Here, two examples of the modelled equation of this study shall be solved using the proposed method with the incorporation of the computed solutions of the lag and volatility terms using the sequences formulated by 16 to obtain the approximate solutions of dIR(t)

Numerical Examples

Example 1

Exact Solution IR(t) = 1 + e-3t

Example 2

Exact Solution IR(t) = sin?(t)

Result and Discussion

The performance of the proposed method (2HBAMM) over other existing methods are determined by computing the exact solution, numerical solution, absolute random errors of the modeled equation (2) and the absolute random errors of other existing methods. The computed results are presented in tables 1 to 2:

Table 1: Performance of 2HBAMM on Example 1

t | Exact | Numerical | Absolute Random | Absolute Random | Absolute Random |

1 | 0.990049834 | 0.990049781 | 5.27492E-08 | 4.44E-04 | 1.51328E-06 |

2 | 0.980198673 | 0.980198692 | 1.83932E-08 | 3.01E-03 | 2.42656E-06 |

3 | 0.970445534 | 0.970445525 | 9.04851E-09 | 9.08E-02 | 6.29916E-06 |

4 | 0.960789439 | 0.960789427 | 1.23523E-08 | 1.18E-04 | 8.37204E-06 |

5 | 0.951229425 | 0.951229458 | 3.35993E-08 | 1.01E-04 | 1.46024E-05 |

6 | 0.941764534 | 0.941764521 | 1.28842E-08 | 2.14E-04 | 1.7834E-05 |

7 | 0.93239382 | 0.932393827 | 7.19405E-09 | 3.92E-03 | 2.64197E-05 |

8 | 0.923116346 | 0.923116342 | 3.98664E-09 | 1.61E-03 | 3.08088E-05 |

9 | 0.913931185 | 0.913931178 | 6.87123E-09 | 3.42E-03 | 4.17463E-05 |

10 | 0.904837418 | 0.904837424 | 6.26404E-09 | 1.15E-04 | 4.72911E-05 |

11 | 0.895834135 | 0.895834135 | 3.47178E-12 | 1.24E-05 | 6.05761E-05 |

12 | 0.886920437 | 0.88692043 | 7.11716E-09 | 8.18E-04 | 6.72745E-05 |

Table 2: Performance of 2HBAMM on Example 2

t | Exact Solution | Numerical Solution | Absolute Random | Absolute Random | Absolute Random |

1 | 1.970445534 | 1.970448149 | 2.61545E-06 | 2.24E-05 | 3.62E-04 |

2 | 1.941764534 | 1.941764203 | 3.30584E-07 | 5.40E-04 | 1.83E-04 |

3 | 1.913931185 | 1.913931359 | 1.73729E-07 | 6.08E-03 | 4.22E-03 |

4 | 1.886920437 | 1.886922874 | 2.43728E-06 | 3.28E-04 | 7.20E-02 |

5 | 1.860707976 | 1.860707673 | 3.03425E-07 | 2.21E-04 | 6.02E-04 |

6 | 1.835270211 | 1.835270327 | 1.15589E-07 | 6.34E-05 | 4.26E-05 |

7 | 1.810584246 | 1.810587578 | 3.33203E-06 | 2.29E-02 | 3.30E-05 |

8 | 1.786627861 | 1.786627445 | 4.16067E-07 | 6.12E-04 | 2.10E-04 |

9 | 1.763379494 | 1.763379634 | 1.39663E-07 | 5.32E-03 | 2.42E-03 |

10 | 1.740818221 | 1.74082047 | 2.24932E-06 | 7.15E-05 | 3.47E-03 |

11 | 1.718923733 | 1.718923448 | 2.85432E-07 | 1.56E-05 | 1.61E-05 |

12 | 1.697676326 | 1.697676407 | 8.0929E-08 | 5.13E-03 | 1.67E-04 |

The results obtained after the numerical implementation of the method in solving some Advanced Stochastic Time-Delay Differential Equation (ASTDDE) as presented in the tables above shown the numerical representation of alternating or stochastic investment returns of the insurance industry caused by the adverse effect of economic fluctuations such as turbulence in inflation rate, human development index, volatility in gross domestic product (GDP) of a country due to fire-brigade approach in new policy implementations and currency-exchange rates on policyholders trust and patronage. Relating our results to other existing results in the literature, comparisons of the Absolute Random Errors (AREs) were carried out which ascertained the advantage of our method over other existing methods in [11-12] in terms of efficiency and accuracy. The proposed method performed better than existing methods in literature by producing the Minimum Absolute Random Errors (MAREs) as presented in table 1 and table 2 for numerical solution of ASTDDEs.

Conclusion and Recommendation

This study has expressed and proffers solutions to the adverse effects of economic fluctuations on the investment returns of insurance industry caused by macroeconomic indicators. The study have also demonstrated that two-step Hybrid Block Adams Moulton Methods (2HBAMM) with the new formulated sequences in literature for computation of the lag and volatility terms is suitable for solving some Advanced Stochastic Time-Delay Differential Equation (ASTDDE) numerically and gives a better result over the existing results in literature which used interpolation approach in computing the lag and the volatility terms. The lower the Absolute Random Error (ARE) of the modeled equation (2), the lower the economic fluctuations which increase the policyholders trust and patronage thereby influencing an increase in the investment returns of the insurance industry and vice versa. Therefore, this study recommends that insurance industry in Nigeria should prioritize the protection of policyholders’ trust whose patronage influences its investment returns by ensuring clarity and transparency in their service delivery. Adequate implementation of price control measure by the government of the day can cushion the adverse effects of economic fluctuations as a result of turbulence in inflation rate, human development index, volatility in gross domestic product (GDP) of a country due to fire-brigade approach in new policy implementations and currency-exchange rates. Future studies should be looked-into for step numbers

Acknowledgement

Acknowledgement goes to the research team of this manuscript for initiating and carrying-out the innovation behind this great research work.

Funding Sources

There is no funding or financial support for this research work.

Conflict of Interest

The authors declare no conflict of interest.

References

- Stefan, A., Galina, H. U.S Monetary Policy and Fluctuations of International Bank Lending. The Economic Implication of Fuel Subsidy Removal in Nigeria. Journal of International Money and Finance, Elsevier, 95(C), 251–268, (2019).

CrossRef - Zakari, M. The Impact of Exchange Rate Fluctuation on Foreign Direct Investment in Nigeria. Journal of Finance and Accounting, 5(4), 165-170, (2017).

CrossRef - Peng, W, Lixia, C, Ye, L (2023). Factors and key problems influencing insured’s poor perceptions of convenience of basic medical insurance: a mixed methods research of a northern city in China. National Library of Medicine, 1066, (2023).

- E. Robinson, E. Trust and Confidence in the Insurance Industry: A Comparative Analysis. Journal of Insurance Studies, 17(1), 55-68, (2019).

- Brown, A & Williamson, B. Understanding Policyholder Satisfaction in the Context of Claims Resolution. Journal of Insurance Studies, 15(2), 87-104, (2019).

- Cristea, M, Marcu, N & Carstina, S. The relationship between insurance and economic growth in Romania compared to the main results in Europe: A theoretical and empirical analysis‘, Procedia Economic Finance, 8 (14), 226-235, (2014).

CrossRef - Shennaev, M. Kh. Regulation of Investment Activities of Insurers. Asian Journal of Multidimensional Research (AJMR), 9 (11), 55-59, (2020).

CrossRef - Lyndon, E. M. Insurance Sector Development and Economic Growth in Nigeria: An Empirical Analysis. Business Economics, (2019).

- Evelyn, B. Introduction to the Numerical Analysis of Stochastic Delay Differential Equations. Journal of Computational and Applied Mathematics, 125, 297-307, (2000).

CrossRef - Ugbebor, O. O. MATH 352 Probability Distribution and Elementary Limit Theorems Published by: The Department of Adult Education, University of Ibadan, Ibadan, (1991).

- Akhtari, B., Babolian, E., Neuenkirch, A. An Euler Scheme for Stochastic Delay Di?erential Equations on Unbounded Domains: Pathwise Convergence. Discrete Contin.Dyn. Syst., Ser.B, 20(1), 23–38, (2015).

CrossRef - Wang, X., Gan, S. The Improved Split-step Backward Euler Method for Stochastic Di?erential Delay Equations .Int. J. Comput. Math., 88(11), 2359–2378, (2011).

CrossRef - Zhang, H. Gan, S., Hu, L. The Split-step Backward Euler Method for Linear Stochastic Delay Deferential Equations. Comput. Appl. Math., 225(2), 558–568, (2009).

CrossRef - Bahar, A. Numerical Solution of Stochastic State-dependent Delay Differential Equations: Convergence and Stability. Advances in Deference Equations, A Springer Open Journal.396 https://doi.org/10.1186/s13662-019-2323-x, 12(7), 1-24, (2019).

CrossRef - Osu, B. O, Amadi, I. U, Azor, P. A. Analytical Solution of Time-Varying Investment Returns with Random Parameters. Sebha University Journal of Pure & Applied Sciences. DOI: 10.51984/JOPAS.V21I2.1857, 21(2), 6-11, (2023).

CrossRef - Osu, B. O., Chibuisi, C., Olunkwa, C & Chikwe, C. F. Evaluation of Delay Term and Noise Term for Approximate Solution of Stochastic Delay Differential Equation without Interpolation Techniques, Global Journal of Engineering and Technology [GJET], 2(9), 1-19., (2023).

- Chibuisi, C., Osu, B. O., Edeki, S. O., Akinlabi, G. O., Olunkwa, C & Ogundile, O. P. Implementation of Two-step Hybrid Block Adams Moulton Solution Methods for First Order Delay Differential Equations Journal of Physics: Conference Series 2199 (2022) 012017. IOP Publishing: DOI:10.1088/1742-6596/2199/1/012017. 1-13, (2022).

CrossRef - Sirisena, U. W., Yakubu, S. Y. Solving delay differential equation using reformulated backward differentiation methods, Journal of Advances in Mathematics and Computer Science, 32(2), 1-15, (2019).

CrossRef - Lambert, J. D. Computational Methods in Ordinary Differential Equations, New York, USA. John Willey and Sons Inc, (1973).

- Dahlquist, G. Convergence and Stability in the Numerical Integration of Ordinary Differential Equations, Math, Scand, 4(2), 33-53, (1956).

CrossRef

This work is licensed under a Creative Commons Attribution 4.0 International License.